BaaS: The cool new acronym on the block

On lithium-ion batteries and NIO's quest to incubate the future of electric vehicle

Hummer owners...come back in two weeks. This one isn’t for you.

Today, the electric vehicle (EV) revolution is well underway, and for good reason.

Even independent of fad quality and the feel-good merits of tempering non-renewable fuel reliance, there are manifold reasons behind the appeal of EVs to both the firm and the consumer of the future.

Among other things, they are quiet, responsive, generate impressive amounts of torque, luxurious (in many cases), and fundamentally aligned with electronic systems, which in turn enables remote management, as well as broader participation in the IoT that underpins adjacent auto technologies like automation.

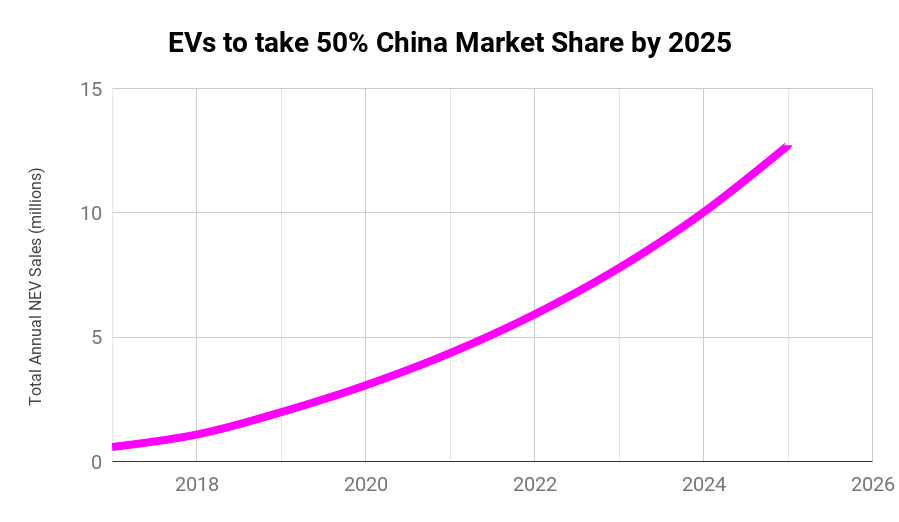

The potential here is absolutely staggering. And ostensibly, it looks set to be realized with minimal opposition. But don’t take my word for it. Check this out:

At the core of this growth story is a single lifeblood: the lithium-ion battery.

Economies of scale and competition associated with the ‘massification’ of such batteries are responsible for the rapid dropping of EV prices around the world, as you can see below. And on the surface, this is the perfect setup for the revolution to begin its assault on the enormous TAM that you see in the figure above.

This, though, is wishful thinking. Looking more critically at lithium-ion batteries as assets in their own rights, clear limitations become apparent - they are demanding of infrastructure, degradable in quality, and depreciative in value. They are essentially sunk costs upon their purchase, making owning an EV a luxury most appropriate for those who can justify not only paying for an EV in the first place, but also finding access to a charging setup and accepting the limited lifespan and decreasing efficiency of the most fundamental component of their new asset.

All of a sudden, then, the road ahead for EVs appears bifurcated between a dead end, of focusing too narrowly on reducing battery costs without addressing more fundamental challenges to their use, and a longer, but more promising route — namely, pausing to ensure that the ecosystem that underpins the EV revolution is robust enough to support it, especially in the densely populated, bureaucratic, infrastructurally underserved, and verticalized emerging markets where much of the remaining TAM lies.

Perhaps fittingly, the Chinese market seems to have found an exemplary response. Launched tentatively in 2020, NIO’s Battery-as-a-Service (BaaS) model treats batteries as swappable modules, thereby eliminating the need for a regular charging station, smoothing out the incidence of the effects of battery degradation, and invalidating the concept of ‘owning’ a depreciative battery asset in the first place. In the same way that SaaS relieved firms and individuals of the stress of constantly updating heavy, legacy systems while still bearing unnecessary fixed costs, enter BaaS to save the day here.

In this article, my endeavor is to present the massive, replicable and disruptive potential of NIO’s BaaS offering - as infrastructure, and as technology. En route, I’ll take you (quickly!) through how the lithium-ion battery works, how its limitations manifest, and finally, how BaaS economics have the potential to spark a meta-revolution within the world of EVs, in emerging and developed markets alike.

How do lithium-ion batteries work?

Time for a quick high-school physics throwback.

At its most basic level, the lithium-ion battery itself consists of several individual power ‘engines’, if you will, called cells. Within each cell, there are three key components:

Positive electrode (connected to the positive terminal of the battery) - usually made of a lithium-containing compound like lithium-cobalt oxide, or lithium iron phosphate

Negative electrode (connected to the negative terminal of the battery) - usually made of carbon

Electrolyte - usually a lithium salt-containing solution

Each component has a key role in the following two processes. In abstract, here’s what they look like:

Charging: When the battery is charging (in a car, this typically takes place while hooked up to a charger overnight), the positive electrode ‘gives up’ some lithium ions. These ions then pass through the electrolyte solution into the negative electrode. Electrons move in the opposite direction as ions. In this case, the movement/current of electrons represents the flow of energy for the battery to store.

Discharging: When the battery is discharging (in other words, when it is in use), the negative electrode simply ‘returns’ the lithium ions it received from the positive electrode. Electrons, as always, move in the opposite direction as these ions - in this direction, their movement/current represents the flow of energy for the battery to use.

To better visualize this process, check this great graphic out:

What are some of the key issues with these batteries?

If there’s one conclusion you should have drawn from the previous section, it should be that these batteries represent massive improvements over incendiary, gas-guzzling engines. But like most rising stars, they’re capable of being real divas.

On an individual level, careful preservation is required to keep them running both safely and efficiently within the cars that they power.

In a broader sense, meanwhile, they are (for now) still underlings to traditional gasoline-powered vehicles (global market share won’t cross the 50% mark for years yet). This gives rise to a truly vicious circle, wherein governments around the world are reluctant to invest in broadly accessible charging infrastructure until fully convinced that EVs will truly become the norm, while EVs cannot, practically speaking, become the norm until consumers are convinced that they would be properly supported.

I hope you’re getting the picture. But for further clarity, here are some specific thoughts on the three biggest barriers that I perceive as serving as deterrents to prospective owners of EVs, particularly in emerging markets:

Lack of charging infrastructure

It goes without saying that charging an EV is a much more difficult undertaking than filling a tank with gas. Charging durations are longer (meaning that drivers have to work a protracted ‘refueling’ experience into their daily driving activities), the scope for technical issues is much greater, and most fundamentally, the availability of charging setups is highly limited, particularly in dense, vertical, urbanized cities where both the land and the regulatory leeway required for such setups comes at a premium. There is also a defining question in play — who should be responsible for providing this infrastructure? Answers vary from economy to economy, and generally tend to be split evenly between vehicle manufacturers, federal governments, utilities companies, and even external fuel providers. But no one source is universally accepted.

At this stage, I want to avoid spoilers…but one of the reasons why I’m so excited about NIO’s BaaS model is that it subverts the need for EV drivers to worry about finding a charging station at all. More on that in a bit.Battery degradation

Given the physical and chemical sensitivity of lithium-ion battery systems, degradation over time and use is to be expected. And admittedly, huge strides have been made in recent years with regards to extending the drivable range of fully-charged EVs — early Nissan models in 2012 had an estimated range of 82 miles per charge upon purchase (which declined by up to 20% by the 5-year mark), whereas most current vehicles operate around the 300-mile mark upon purchase, with range degradation of 10% discernible only after ~120000 miles or more. Moreover, as Deloitte’s 2020 Global Automotive Consumer Study indicates, most people demand more range from their EVs than they actually need — participants drove an average of 27 miles a day, yet over 60% of them indicated that they would prefer for an EV they owned to have a minimum single-charge range of 200-400 miles.

Unfortunately, consumer naivety (fickleness? immaturity?) is a huge factor in the automotive industry. And to be fair, the notion that a fundamental component of one’s car is disintegrating not only with use, but also with extreme weather (cold weather affects energy storage, while heat results in battery stress during the use of energy) and even extreme charge levels (batteries left idle overnight at 0% or 100% will degrade more than ‘moderately’ charged batteries), is an understandably uncomfortable one for prospective owners.This graphic from Battery University does a good job at showing how rapidly EV batteries in general can disintegrate, the more cycles (trips) they are used towards.

High fixed and variable costs

Right off the bat, the initial purchase price for an EV is typically higher than that of a traditionally fueled/ICE vehicle. Add to this the notion that the whole asset is depreciating rapidly (driven by battery degradation), and the high utility costs that make charging expensive, and you begin to understand why EVs are still viewed as a luxury buy by so many. The International Council on Clean Transportation forecasts that price parity between EVs and traditional vehicles will be achieved - across sedans, crossovers and SUVs - by 2025. And tax incentives are available across the board. But for now, the idea of willingly taking on the incidence of what is in many ways an unsupported sunk cost is a prohibitive one in many parts of the world.

So…what if there was something that tackled each of these three issues — that is, invalidated the need for personal access to charging infrastructure, took the onus of caring for a high-maintenance, fickle lithium-ion battery out of consumers’ hands, and made EVs cheaper to purchase in the first place? Time for the fun part.

The BaaS Story

In telling the BaaS story, it merits first establishing why China is such an apt location for a successful dry run.

For one, EV penetration in China - the world’s single largest automotive market - is currently at an optimal level, wherein the present and future look bright, but there is plenty left to do in order to hit the (sustainability-motivated) goals that the government has set. As of now, there are a little over 2.5 million EVs in China (vs around 1 million in Europe, and 0.9 million in the US). During the pandemic-riddled month of September 2020 alone, 125000 new EVs were sold nationwide. And the growth story is expected to roll on — CAGR is projected at 31% through 2028, boosted by increases in government subsidies, as well as pressure from the other direction in the form of increasingly stringent emissions regulations.

Enter NIO to raise its trajectory.

Founded in November 2014 and headquartered in Shanghai, NIO went public in the US in 2018. Its non-EV interests span autonomous driving (via research through the NIO Pilot program, which is expected to launch a Level 4 car, complete with lane keeping, cruise control and other self-driving traits, by 2022), clothing and service centers. Its core offerings are a current suite of 4 cars - EP9, EC6, ES6 and ES8 - with 4 more expected to launch over coming quarters.

Their most interesting line of business, though, is NIO Power. This is the division under whose auspices NIO’s forays into BaaS have been incubated.

What is BaaS?

Simply speaking, BaaS is to cars what SaaS is to companies. It refers to the principle of separating the vehicle from the battery that powers it, or put differently, the principle of turning the battery into a ‘subscribable’ component, starting at just $142/month for an entry-level variant. With BaaS, instead of charging your existing battery, you just ‘grab’ a new one as and when you need it.

The core capability that underlies BaaS is battery swapping. One of NIO’s key design foci has been to ensure that all of their cars - whether 70kWh or 100kWh models - have the same battery trays. In other words, any of their cars are technically compatible with any of their batteries. This makes swapping easy, and also means that consumers are not rendered ‘legacy’ the moment NIO develops new batteries — even older NIO vehicles can house them. From NIO’s perspective, this cross-compatibility presents an easy and compelling upsell opportunity, whereby they can rake in the premiums of new and improved battery products without needing to launch a new vehicle in tandem.

When it comes to the size of the swapping operation, NIO’s reach is already massive. As of now, they have upwards of 143 ‘swapping stations’ across China, and complete upwards of 4000 battery swaps every day — as things stand, a total of more than 1 million battery swaps have been completed at NIO stations. For their part, these stations charge several batteries at once, and can complete swaps quickly, eliminating any need for the consumer to worry at all about the battery in their car at the time — when they pass a station, they can simply, rapidly replace it with one that is ready to go, and leave the old one at the station for NIO to deal with.

Most interestingly, like the batteries they help to service, these stations themselves are modular, in the sense that they can be easily relocated based on demand. Wherever NIO’s business concentrates most heavily is where such stations will be most plentifully found.

Disruptive potential

With regards to how it can disrupt legacy EV practices, the impacts of the BaaS model are best visualized within the 3-problem framework I proposed earlier:

Lack of charging infrastructure

Simply, this isn’t an individual problem anymore, because for around a couple hundred dollars a month (or in other terms, less than 1/1000 the price of a new NIO car), customers can simply pass the buck onto NIO. The driving experience is returned to the quasi simplicity of setting off, spending a couple of minutes refreshing your car’s power (if you even need to) when you pass by what is essentially a proxy for a highway gas station, and then continuing on your journey.

I wish you would let it be that simple. This said, you would be within your rights to question whether this actually represents an improvement, given that in setting up their own charging operations, NIO itself would face at least similar spatial and regulatory constraints to those aforementioned. In addressing this concern, it helps to think from the perspective of the Chinese government, who in many ways have to choose the lesser of two ‘evils’ en route to facilitating the broader trend EV penetration that would best complement the nation’s sustainability goals. With this in mind, the notion of helping (via subsidies, province-level approvals etc.) an avant-garde auto brand (don’t sleep on how much every market wants their own ‘Tesla’-esque poster child) to build out a modular, adjustable, democratic network of swap stations, in response to clear demand for a novel program, is far more attractive than using public money to set up scores of individual charging stations and then hoping that this motivates, rather than concurrently supports, an increased interest and belief in EVs.

Battery degradation

One of the core consumer benefits of BaaS is the ability to instantaneously switch over to using a battery that has essentially been quality-guaranteed mere seconds ago — by virtue of being handed over at a station by a representative of none other than NIO itself. From a safety standpoint, concerns are completely assuaged, and performance parity guaranteed.

The vehicle-battery separation that characterizes BaaS has a similar effect on any asset depreciation concerns. Within the BaaS model, a consumer’s only fully-owned asset is the shell of the vehicle itself, which depreciates in value far less quickly than a battery does. Moreover, this separation points to the potential for a roaring second-hand EV market, which in turn is likely to further motivate people in the market for a new car — particularly first-time buyers among the young, burgeoning Chinese middle class — to choose an EV. With BaaS, the sunk cost fear of old is no more.

This separation carries huge value from NIO’s perspective too. By keeping it ‘in-house’ (that is, within NIO’s own supply chain), NIO retains control over the battery’s lifecycle. Now typically, when a lithium-ion battery degrades beyond usability in an EV, it is abandoned; car owners typically have no viable use cases for such a battery, and equally limited access to markets full of people who might. NIO, on the other hand, can tap into an institutional network of resale markets, consisting of firms manufacturing everything from electric scooters to storage systems, each of which rely on lithium-ion technology, but have nowhere near the same energy requirements that EVs do. In this way, NIO is not only insulating its customers from the ills of battery degradation, but also fashioning a very viable (if retroactive) route toward improved margins of their own.

High fixed and variable costs

NIO solves this particular problem with extremely competitive pricing. For one, opting for BaaS instantly shaves at least RMB 70000 (or around ~20%) off the price of a NIO vehicle — doing the math on the monthly battery-subscription fee of around RMB 1000 (minus savings on battery maintenance, of course), and the enduring appeal to consumers becomes clear. To sweeten the deal further, Chinese laws dictate that EVs priced above RMB 300000 (as all of NIO’s are, given their efforts to brand as a Tesla-like luxury player) are only eligible for federal subsidies if they are compatible with some sort of battery-swapping program.

By way of a quick recap at this point, the BaaS model attenuates two key EV usage issues (in charging and battery degradation), while fundamentally lowering the economic and psychological barriers to buying one in the first place.

Tailwinds: What’s buoying NIO’s incubation of the BaaS model?

Government: EV use in China is soaring, and the government is playing ball, chasing a minimum of 25% penetration by 2025. This would be no mean achievement in the world’s largest auto market, but judging by the amount of credit being extended to EV buyers (subsidies totaled upwards of $1.4 billion in Q1 of 2020), a real attempt is being made. People are increasingly becoming buyers as a function of the pandemic-inspired shift away from ride-sharing, so this could not have come at a better time.

Marketing: Like with any novel undertaking of this kind, the buzz alone is doing great things for NIO. For its part, NIO has set the stage perfectly over previous years, branding itself as a best-in-class, exclusive, luxury offering with the goal of attaining an almost cult-like following (maybe this is my inner car fanboy talking, but just look at the curves on the recently launched ET-7 below. Forget that it also comes with LIDAR and a ~600-mile range. It’s sexy.). Indeed, while it may seem that a business model like BaaS, within which cost-cutting stands out as a major benefit, may contribute to the dilution of a luxury image, the reality is that NIO are building a Tesla-like brand — one which made its name by astutely betting on the initial fad quality of EVs, but also one which is branching out into the mass-market at the perfect time.

Product: As I mentioned earlier, NIO is by no means resting on the laurels of its existing range of cars. The BaaS model will constantly have new life breathed into it by a rapidly expanding portfolio of products, with at least 4 new models slated to be launched in the next 2 years. While the focus of this article is decidedly not to advocate for NIO as an investment (or even a car maker of choice), BaaS presents NIO with a major first-mover advantage. Evidently, they are planning to milk this massively, and will undoubtedly engineer the timelines of these launches in order to most optimally compete across price points. Indeed, at the end of the day, the point here is simple — consistently introducing the world to quality new cars cannot hurt their endeavor to call more attention to the way in which they support those cars.

Headwinds and Mitigants: The road to the BaaS model’s next big move

Scale: The biggest questions asked of Tesla were about their ability to scale. Many people who answered those questions (as seen below), did so very prematurely. I think we can all agree that Tesla has done fine (as for their future, ask Cathie Wood). In this case, a couple of key ideas underscore the sustainable nature of the growth story that NIO (and therefore the BaaS model) are only just embarking on. Firstly, EVs are far less of an unknown quantity than they were when scalability questions could reasonably be asked. Even if the luxury/fad tag persists, innovations like BaaS are forcing people to see EVs as the environmentally, practically and commercially viable products that they are. Secondly, having China as an incubator for a potentially global innovation is seldom a bad thing. And this is particularly true of EV-related innovation, given that most battery components are produced in China (which controls 51% of the world’s supply of chemical lithium, vs 2% in the US, as well as 62% of all chemical cobalt, and 100% of spherical graphite), while NIO has been able to rack up nearly 1200 battery swapping-related patents. Ultimately, to every skeptic who doubts that an innovation polished in the Chinese market could truly become world-class, I raise the question: if a seemingly dispensable, tree-hugging ‘luxury’ brand can secure commercial and regulatory buy-in in China, why the hell shouldn’t it work elsewhere? I’m sure there are compelling answers to that question. And BaaS has been tried before, extremely unsuccessfully. But the fact is that scars from attempts made in 2013, long before EVs even gestured at entering their prime — and attempts that also weren’t tied closely enough to consumer trends or branding — cannot and should not be a deterrent in 2021.

Saturation Concerns: Quite honestly, NIO is not without high-quality competitors in the avant-garde automotive space - companies like Xiaopeng, Li Auto and even established players like Volkswagen, Volvo and Tesla spring to mind. This said, NIO is carving out a niche, and one that is defined by BaaS. My logic here is that the combination of brand name (boosted by NIO being publicly traded), luxury and low prices that characterizes NIO’s niche should lead to great success in both Chinese and international markets. And if competitors anywhere in the world choose to follow NIO’s lead, I personally wouldn’t mind (like I said, this isn’t about NIO!), because in doing so, they would be compelled to try and replicate the company’s most daring innovation, which is none other than the BaaS model. In any event, the point I’m making is that company-level competition is a fantastic thing for BaaS, and therefore for EV penetration in general. NIO itself be damned. Shoot the messenger for all I care.

Government (Ep. 2): The Chinese government is playing ball for now, but will this remain the case? For the next two years at least, the answer is yes. At a federal level, EV subsidies are guaranteed to remain in force until at least 2022; indeed, post-COVID, when sustainability can return from the fringes of policy priority, there is no reason why such systems won’t be renewed if not further bolstered as well. At a provincial level, meanwhile (which is important to consider, given that most infrastructure-related EV policymaking is done on a province-by-province basis), there is also no reason for alarm — NIO has quickly embedded itself into the frontier of the EV movement in China, forging relationships with regulators and governments alike that should stand the firm (and its poster child of a business model) in wonderful stead. This particular aspect is a positive example of the big getting bigger.

This has definitely been one of the more abstract and thematic pieces I’ll subject you to (promise!), but I hope three things are clear:

The EV revolution is well underway, but there is still ample room to go.

Key to tapping unaddressed markets will be dealing with three battery-related concerns: infrastructure, degradation and cost.

The jury is technically still out on BaaS, but I think it has the potential to change the auto industry as we know it.

For now, this is goodbye. I’d welcome your thoughts in the comments.

Other Sources:

https://www.geotab.com/white-paper/barriers-to-ev-adoption/

https://www.electronics-notes.com/articles/electronic_components/battery-technology/li-ion-lithium-ion-advantages-disadvantages.php

https://www.voanews.com/silicon-valley-technology/how-china-dominates-global-battery-supply-chain

https://www.explainthatstuff.com/how-lithium-ion-batteries-work.html

https://hbr.org/2015/04/why-tesla-wont-be-able-to-scale